Even if the total amount owed or the monthly payments are not prohibitive, the demands of managing multiple loans can get in the way of your day-to-day operations—and your ability to grow.

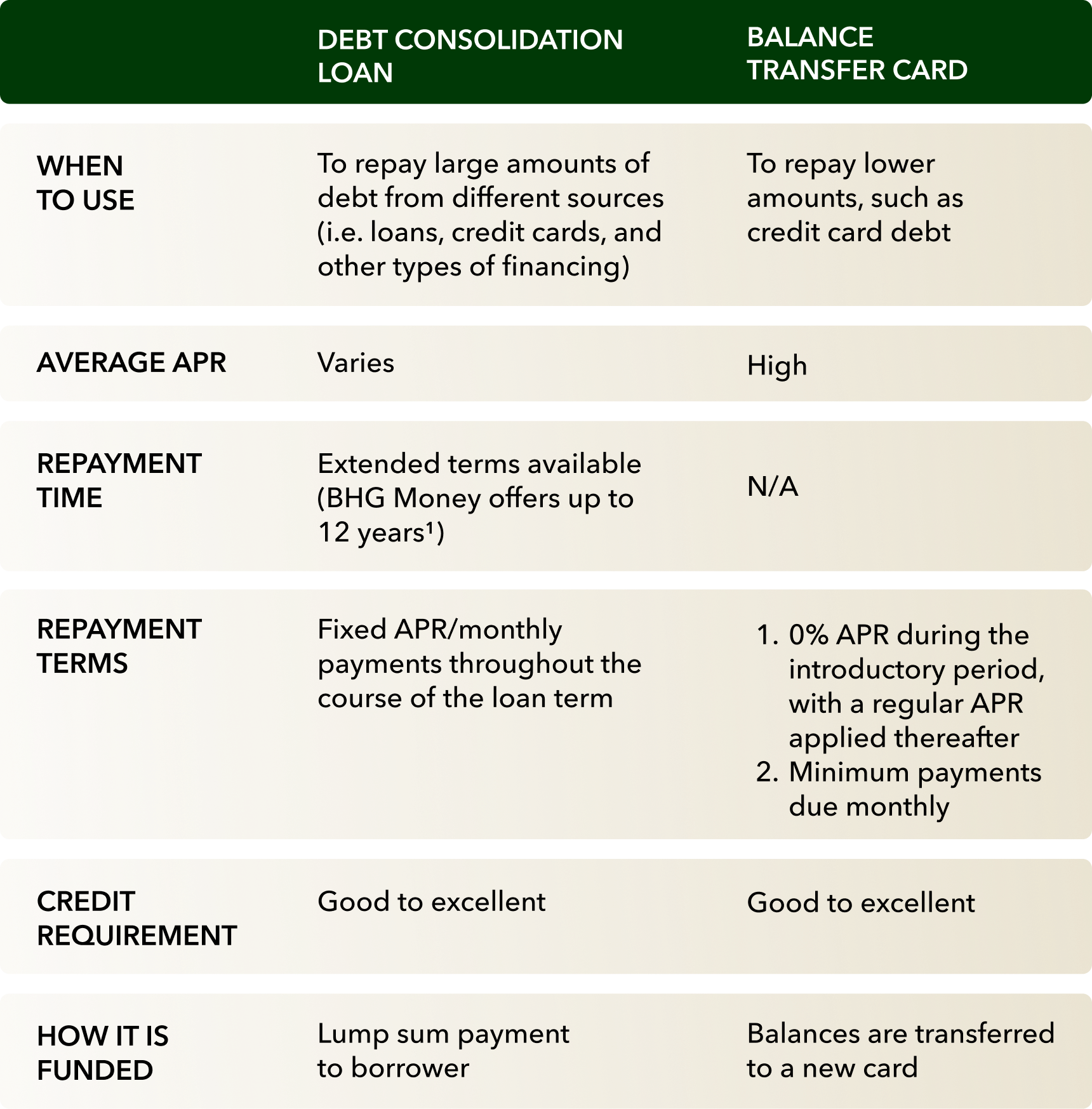

Balance transfer cards and debt consolidation loans are effective in different situations, but they provide one overarching benefit: They ease the financial burden of complex debt structures on business owners.

Further, if you choose to partner with BHG Money, our large loan amounts and extended terms1 allow you to consolidate debt, reduce your monthly payments, and utilize additional funds for operational improvements.

You can learn more about our financial solutions and view your personalized estimate here. It only takes 30 seconds.

Other financing options to help you restructure business debt, strategically

While balance transfer cards and debt consolidation loans are your primary tools for reorganizing debt, there are other financing options available that can be helpful in certain situations.

For example, you may consider a business line of credit, which gives the borrower a revolving credit line that they can borrow against whenever they need. A line of credit provides access to funding with interest only being charged on the amount borrowed rather than on the entire amount available. This financing solution is generally used to cover immediate expenses but can also be leveraged to pay off outstanding debts.

Refinancing is another option. Refinancing is similar to consolidating business debt, so much so that the two terms are often used interchangeably. Typically, refinancing is the process of taking out a new loan that pays off the debt of the previous one, whereas debt consolidation for business owners involves combining multiple loans into a new financial solution.

What are the advantages of a debt consolidation loan from BHG Money?

BHG Money provides large debt consolidation loans up to $500,0001,2 so that you can pay off debt and invest additional funds into your business. Plus, our longer repayment terms of up to 12 years1 give you affordable monthly payments.

Compared to traditional lenders, BHG Money can provide the funding you want when you want it. So, if you’re ready to strategically restructure your existing debt, our team is prepared to serve your needs—on your schedule—with dedicated loan specialists available 7 days a week.

Get started online by viewing your monthly payment estimate here.

¹ Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Finance amount may vary depending on the applicant's state of residence. Call for complete program details.

² BHG Money business loans typically range from $20,000 to $250,000; however, well-qualified borrowers may be eligible for business loans up to $500,000.

For California Residents: BHG Money loans made or arranged pursuant to a California Financing Law license - Number 603G493.

No application fees, commitment, or impact on personal credit to estimate your payment.